Chapter 03: Multi-Series Fitting#

This notebook demonstrates one of vangja’s key features: vectorized multi-series fitting. Unlike Facebook Prophet, which fits time series one at a time, vangja can fit multiple time series simultaneously using vectorized computations.

We’ll compare two approaches:

Sequential fitting (Prophet-style): Fit each time series independently, one after another

Simultaneous fitting (Vangja-style): Fit all time series at once with

pool_type="individual"

Both approaches produce equivalent results when series share the same time range, but the vectorized approach is significantly faster when you have many time series.

Note: For series with different date ranges, see Chapter 04 which covers important caveats.

Setup and Imports#

[1]:

import warnings

warnings.filterwarnings("ignore")

[2]:

import time

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from vangja import FourierSeasonality, LinearTrend

from vangja.datasets import generate_multi_store_data

from vangja.utils import metrics

# Set random seed for reproducibility

np.random.seed(42)

print("Imports successful!")

Imports successful!

Generate Synthetic Multi-Store Data#

We’ll use 5 synthetic time series representing different stores, all sharing the same time range (2015-2020). This is the ideal scenario for simultaneous fitting.

Each series has:

A linear trend with different slopes

Yearly seasonality with different amplitudes

Weekly seasonality

Random noise

Vangja provides generate_multi_store_data() in vangja.datasets for this purpose.

[3]:

# Generate synthetic multi-store data

all_data, series_params = generate_multi_store_data(seed=42)

# Split into individual series for later use

all_series = [

all_data[all_data["series"] == name].reset_index(drop=True)

for name in all_data["series"].unique()

]

print(f"Date range: {all_data['ds'].min().date()} to {all_data['ds'].max().date()}")

print(f"Total days per series: {len(all_series[0])}")

print(f"Number of series: {len(all_series)}")

Date range: 2015-01-01 to 2019-12-31

Total days per series: 1826

Number of series: 5

[4]:

# Display series information

for params in series_params:

series_df = all_data[all_data["series"] == params["name"]]

print(

f"{params['name']}: {len(series_df)} samples, y range: {series_df['y'].min():.1f} to {series_df['y'].max():.1f}"

)

print(f"\nTotal combined data: {len(all_data)} samples")

store_north: 1826 samples, y range: 61.2 to 232.2

store_south: 1826 samples, y range: 45.0 to 185.2

store_east: 1826 samples, y range: 75.1 to 292.2

store_west: 1826 samples, y range: 66.5 to 166.1

store_central: 1826 samples, y range: 81.0 to 354.4

Total combined data: 9130 samples

[5]:

# Visualize all series

fig, axes = plt.subplots(2, 3, figsize=(15, 8))

axes = axes.flatten()

for i, params in enumerate(series_params):

ax = axes[i]

series_df = all_data[all_data["series"] == params["name"]]

ax.plot(series_df["ds"], series_df["y"], linewidth=0.5, alpha=0.8)

ax.set_title(params["name"])

ax.set_xlabel("Date")

ax.set_ylabel("Value")

ax.grid(True, alpha=0.3)

# Hide the 6th subplot

axes[5].axis("off")

plt.tight_layout()

plt.show()

Prepare Train/Test Splits#

We’ll hold out the last 365 days (1 year) of each series for testing.

[6]:

test_days = 365

train_series = []

test_series = []

for series_df in all_series:

train_series.append(series_df[:-test_days].copy())

test_series.append(series_df[-test_days:].copy())

# Combined training data

train_combined = pd.concat(train_series, ignore_index=True)

print(f"Training data per series: {len(train_series[0])} samples")

print(f"Test data per series: {len(test_series[0])} samples")

print(f"Total training samples: {len(train_combined)}")

Training data per series: 1461 samples

Test data per series: 365 samples

Total training samples: 7305

Approach 1: Sequential Fitting (Prophet-style)#

In the traditional approach (like Facebook Prophet), we fit each time series separately. This means:

Creating a new model instance for each series

Fitting each model independently

Total time = sum of individual fitting times

This approach works fine for a few time series, but becomes slow when you have many series.

[7]:

def create_model():

"""Create an additive model with trend and seasonality."""

return (

LinearTrend(n_changepoints=15)

+ FourierSeasonality(period=365.25, series_order=10)

+ FourierSeasonality(period=7, series_order=3)

)

print(f"Model structure: {create_model()}")

Model structure: LT(n=15,r=0.8,tm=None) + FS(p=365.25,n=10,tm=None) + FS(p=7,n=3,tm=None)

[8]:

# Fit each series sequentially

sequential_models = []

sequential_times = []

print("Sequential fitting:")

total_start = time.time()

for i, (train_df, params) in enumerate(zip(train_series, series_params)):

model = create_model()

start = time.time()

model.fit(train_df, method="mapx")

elapsed = time.time() - start

sequential_times.append(elapsed)

sequential_models.append(model)

print(f" {params['name']}: {elapsed:.2f}s")

total_sequential_time = time.time() - total_start

print(f"\nTotal sequential time: {total_sequential_time:.2f}s")

Sequential fitting:

WARNING:2026-02-27 00:13:25,417:jax._src.xla_bridge:876: An NVIDIA GPU may be present on this machine, but a CUDA-enabled jaxlib is not installed. Falling back to cpu.

store_north: 9.31s

store_south: 2.54s

store_east: 2.57s

store_west: 3.35s

store_central: 2.44s

Total sequential time: 20.21s

[9]:

# Generate predictions and calculate metrics for sequential fitting

sequential_futures = []

sequential_metrics = []

for model, test_df, params in zip(sequential_models, test_series, series_params):

future = model.predict(horizon=test_days, freq="D")

sequential_futures.append(future)

m = metrics(test_df, future, "complete")

m.index = [params["name"]]

sequential_metrics.append(m)

sequential_metrics_df = pd.concat(sequential_metrics)

print("Sequential Fitting Metrics:")

display(sequential_metrics_df)

Sequential Fitting Metrics:

| mse | rmse | mae | mape | |

|---|---|---|---|---|

| store_north | 65.589342 | 8.098725 | 6.450520 | 0.034214 |

| store_south | 40.167320 | 6.337769 | 5.071716 | 0.034952 |

| store_east | 92.251552 | 9.604767 | 7.644443 | 0.033662 |

| store_west | 28.766430 | 5.363435 | 4.284655 | 0.031891 |

| store_central | 131.073982 | 11.448755 | 9.184140 | 0.032899 |

Approach 2: Simultaneous Fitting (Vangja-style)#

Vangja can fit multiple time series simultaneously by:

Combining all series into a single DataFrame with a

seriescolumnUsing

pool_type="individual"so each series gets its own parametersUsing

scale_mode="individual"so each series is scaled independently

This approach leverages vectorized computations in PyMC/JAX, which is significantly faster than fitting models sequentially.

[10]:

def create_model_individual():

"""Create an additive model with individual pooling for multi-series fitting."""

return (

LinearTrend(

n_changepoints=15, pool_type="individual", delta_pool_type="individual"

)

+ FourierSeasonality(period=365.25, series_order=10, pool_type="individual")

+ FourierSeasonality(period=7, series_order=3, pool_type="individual")

)

print(f"Model structure: {create_model_individual()}")

Model structure: LT(n=15,r=0.8,tm=None) + FS(p=365.25,n=10,tm=None) + FS(p=7,n=3,tm=None)

[11]:

# Fit all series simultaneously

model_combined = create_model_individual()

start_time = time.time()

model_combined.fit(train_combined, method="mapx", scale_mode="individual")

time_combined = time.time() - start_time

print(f"Simultaneous fitting time: {time_combined:.2f}s")

print(f"Speedup vs sequential: {total_sequential_time / time_combined:.2f}x")

Simultaneous fitting time: 5.79s

Speedup vs sequential: 3.49x

[12]:

# Generate predictions

future_combined = model_combined.predict(horizon=test_days, freq="D")

print(

f"Prediction columns: {[col for col in future_combined.columns if 'yhat' in col]}"

)

print(f"Group mapping: {model_combined.groups_}")

Prediction columns: ['yhat_0', 'yhat_1', 'yhat_2', 'yhat_3', 'yhat_4']

Group mapping: {0: 'store_central', 1: 'store_east', 2: 'store_north', 3: 'store_south', 4: 'store_west'}

[13]:

# Calculate metrics for simultaneous fitting

# Since all series share the same date range, we can directly use the predictions

simultaneous_metrics = []

for test_df, params in zip(test_series, series_params):

# Find the group code for this series

group_code = [k for k, v in model_combined.groups_.items() if v == params["name"]][

0

]

# Create a future df with the correct column name for metrics()

future_for_metrics = future_combined[["ds", f"yhat_{group_code}"]].copy()

future_for_metrics.columns = ["ds", "yhat_0"]

m = metrics(test_df, future_for_metrics, "complete")

m.index = [params["name"]]

simultaneous_metrics.append(m)

simultaneous_metrics_df = pd.concat(simultaneous_metrics)

print("Simultaneous Fitting Metrics:")

display(simultaneous_metrics_df)

Simultaneous Fitting Metrics:

| mse | rmse | mae | mape | |

|---|---|---|---|---|

| store_north | 65.489176 | 8.092538 | 6.444646 | 0.034175 |

| store_south | 40.012782 | 6.325566 | 5.062452 | 0.034804 |

| store_east | 92.538181 | 9.619677 | 7.663854 | 0.033768 |

| store_west | 28.701616 | 5.357389 | 4.277841 | 0.031851 |

| store_central | 130.820070 | 11.437660 | 9.175294 | 0.032854 |

Comparison of Results#

Let’s compare the two approaches side by side.

[14]:

# Timing comparison

timing_comparison = pd.DataFrame(

{

"Approach": ["Sequential (Prophet-style)", "Simultaneous (Vangja-style)"],

"Time (s)": [total_sequential_time, time_combined],

"Speedup": [1.0, total_sequential_time / time_combined],

}

)

print("Timing Comparison:")

display(timing_comparison)

Timing Comparison:

| Approach | Time (s) | Speedup | |

|---|---|---|---|

| 0 | Sequential (Prophet-style) | 20.214615 | 1.000000 |

| 1 | Simultaneous (Vangja-style) | 5.787260 | 3.492951 |

[15]:

# Metrics comparison

comparison_rows = []

for params in series_params:

name = params["name"]

seq_metrics = sequential_metrics_df.loc[name]

sim_metrics = simultaneous_metrics_df.loc[name]

comparison_rows.append(

{

"Series": name,

"Approach": "Sequential",

"RMSE": seq_metrics["rmse"],

"MAE": seq_metrics["mae"],

"MAPE": seq_metrics["mape"],

}

)

comparison_rows.append(

{

"Series": name,

"Approach": "Simultaneous",

"RMSE": sim_metrics["rmse"],

"MAE": sim_metrics["mae"],

"MAPE": sim_metrics["mape"],

}

)

metrics_comparison = pd.DataFrame(comparison_rows)

print("Metrics Comparison:")

display(metrics_comparison)

Metrics Comparison:

| Series | Approach | RMSE | MAE | MAPE | |

|---|---|---|---|---|---|

| 0 | store_north | Sequential | 8.098725 | 6.450520 | 0.034214 |

| 1 | store_north | Simultaneous | 8.092538 | 6.444646 | 0.034175 |

| 2 | store_south | Sequential | 6.337769 | 5.071716 | 0.034952 |

| 3 | store_south | Simultaneous | 6.325566 | 5.062452 | 0.034804 |

| 4 | store_east | Sequential | 9.604767 | 7.644443 | 0.033662 |

| 5 | store_east | Simultaneous | 9.619677 | 7.663854 | 0.033768 |

| 6 | store_west | Sequential | 5.363435 | 4.284655 | 0.031891 |

| 7 | store_west | Simultaneous | 5.357389 | 4.277841 | 0.031851 |

| 8 | store_central | Sequential | 11.448755 | 9.184140 | 0.032899 |

| 9 | store_central | Simultaneous | 11.437660 | 9.175294 | 0.032854 |

[16]:

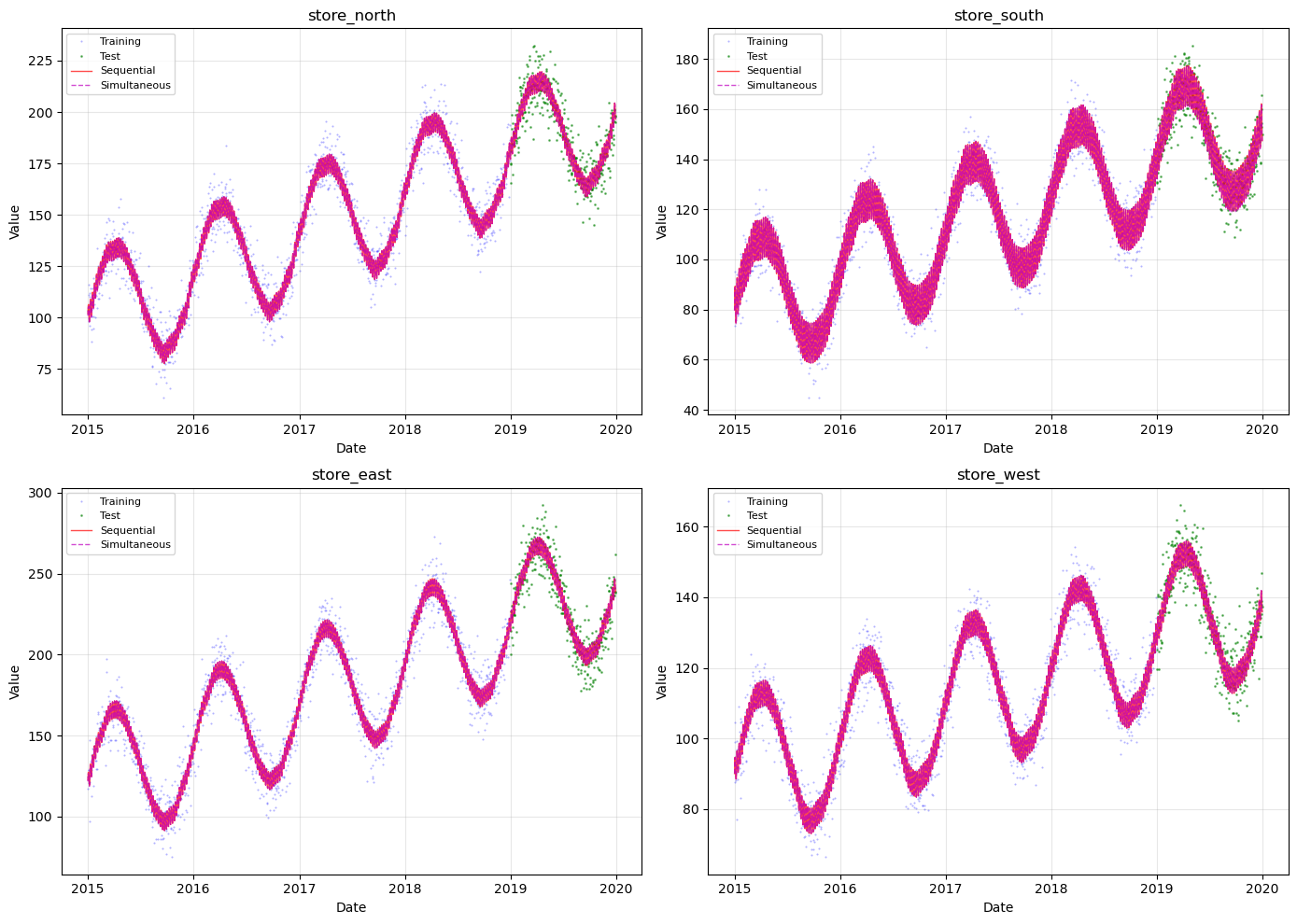

# Visual comparison for a few series

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

axes = axes.flatten()

for i, (ax, params) in enumerate(zip(axes, series_params[:4])):

name = params["name"]

train_df = train_series[i]

test_df = test_series[i]

# Sequential prediction

future_seq = sequential_futures[i]

# Simultaneous prediction

group_code = [k for k, v in model_combined.groups_.items() if v == name][0]

ax.plot(

train_df["ds"], train_df["y"], "b.", markersize=1, alpha=0.3, label="Training"

)

ax.plot(test_df["ds"], test_df["y"], "g.", markersize=2, alpha=0.5, label="Test")

ax.plot(

future_seq["ds"],

future_seq["yhat_0"],

"r-",

linewidth=1,

alpha=0.7,

label="Sequential",

)

ax.plot(

future_combined["ds"],

future_combined[f"yhat_{group_code}"],

"m--",

linewidth=1,

alpha=0.7,

label="Simultaneous",

)

ax.set_title(name)

ax.set_xlabel("Date")

ax.set_ylabel("Value")

ax.legend(loc="upper left", fontsize=8)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Summary#

Key Findings#

Equivalent Results: When all series share the same time range, sequential and simultaneous fitting produce nearly identical results. Small differences are due to optimization randomness.

Significant Speedup: Simultaneous fitting is substantially faster due to:

Single model compilation (vs. N separate compilations)

Vectorized JAX computations across all series

The speedup increases with more time series

Scalability: While we demonstrated with 5 series, vangja can handle hundreds of time series simultaneously, making it ideal for:

Retail demand forecasting (many SKUs)

Energy load forecasting (many meters)

Financial time series (many stocks)

When to Use Simultaneous Fitting#

Scenario |

Recommendation |

|---|---|

Many series, same time range |

✅ Use simultaneous fitting |

Few series (<3) |

Either approach works |

Different model per series |

Use sequential fitting |

Series with different date ranges |

See Chapter 04 for caveats |

Important Caveats#

Simultaneous fitting works best when series share the same time range. When fitting series with very different date ranges (e.g., 1949-1960 vs 2007-2016), there are important considerations:

Changepoint placement: The

n_changepointsare distributed across the entire combined time range, so each individual series may get fewer changepoints than expectedTime normalization: Each series occupies only a portion of

t = [0, 1]Prediction filtering: You must filter predictions to each series’ relevant date range

See Chapter 04: Multi-Series Fitting Caveats for detailed examples and solutions.

What’s Next#

Chapter 04 examines what happens when the time series being fitted simultaneously have different date ranges — a common real-world scenario that introduces subtle but important pitfalls.